Deep dive into Cal-Maine ($CALM)

Cracking the Shell: The Complex World of Eggs

1.0 Introduction

Every once in a while, I stumble upon a company that seems simple, yet, turns out to be incredibly complex. Cal-Maine is one that fits this description.

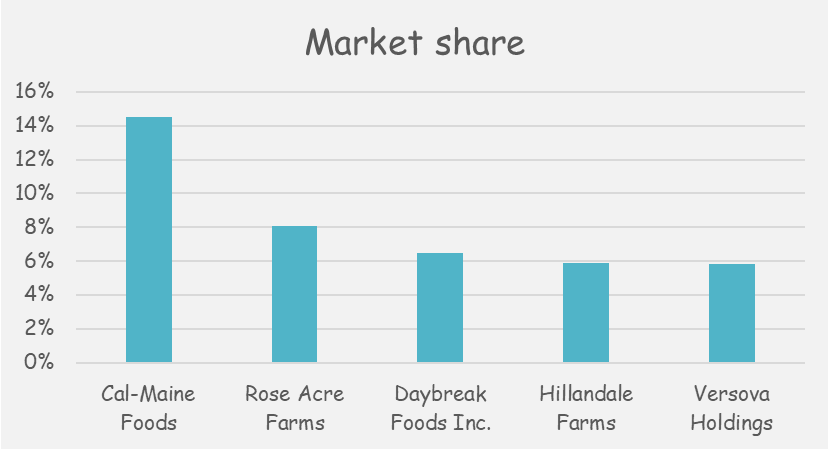

It is the largest producer and distributor of shell eggs in the U.S., and its closest competitor is almost half its size.

Based on the description, one would expect that this is a relatively simple company. I mean, it only sells eggs, right?

What if I told you that the management has very little control over a business of this kind? There’s a lot to unpack, so let’s get started.

2.0 The eggs

In theory, the revenue generated would be equal to the number of eggs sold multiplied by the average egg price. So let’s have a look at these two variables:

Cal-Maine sells two types of eggs:

Specialty - These encompass a broad range of products, such as cage-free, organic, brown, free-range, pasture-raised, and nutritionally enhanced eggs.

Conventional - all other shell eggs

Why is this important? The specialty eggs are typically sold at prices and terms negotiated directly with customers. Unlike conventional, where the wholesale prices are volatile.

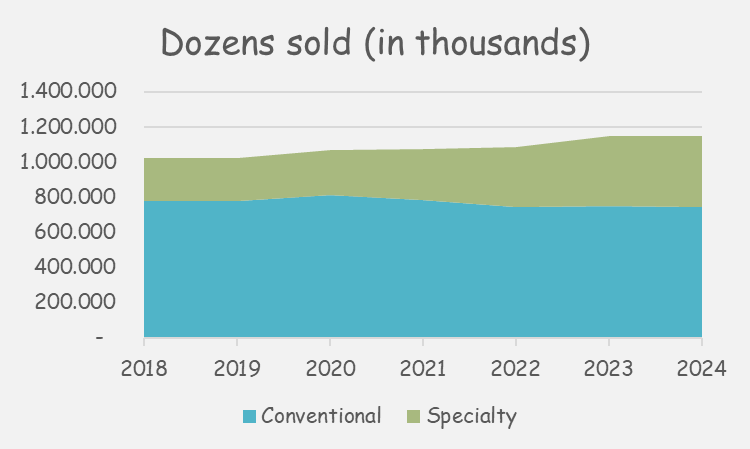

In 2024, the company sold 12% more dozens than back in 2018. This is more impressive than it sounds, as this is not a growing market. The demand for eggs is relatively stable, and it only grows with an increase in population. This indicates the company has slightly increased its market share during this time.

But more importantly, the composition has changed. In 2018, about 244m dozens of specialty eggs were sold. This number increased to 401m in 2024 (+64%)!

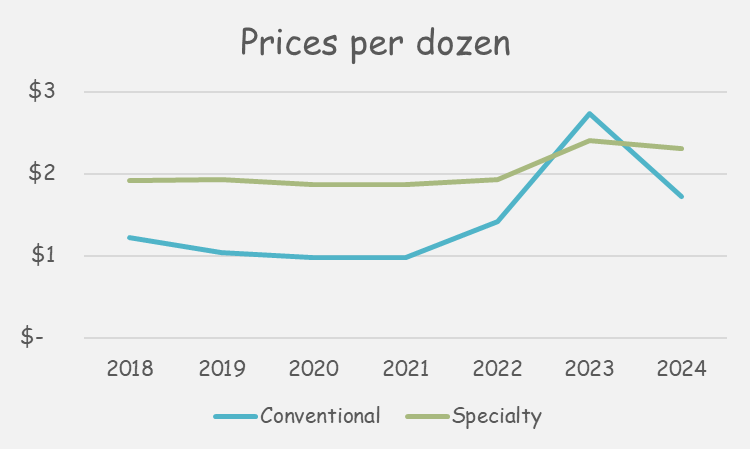

The specialty eggs are not only more expensive, but the price is significantly more stable.

Well, except for 2023. What was that about? Why were conventional eggs more expensive?

The answer is HPAI, known as “Highly Pathogenic Avian Influenza” which is deadly to domestic poultry and can wipe out entire flocks within a matter of days. When there is an HPAI outbreak, there is a significant decrease in supply, which pushes the price up. This is unpredictable, and the only way to deal with this is to mitigate the risk by having multiple locations, something that Cal-Maine has.

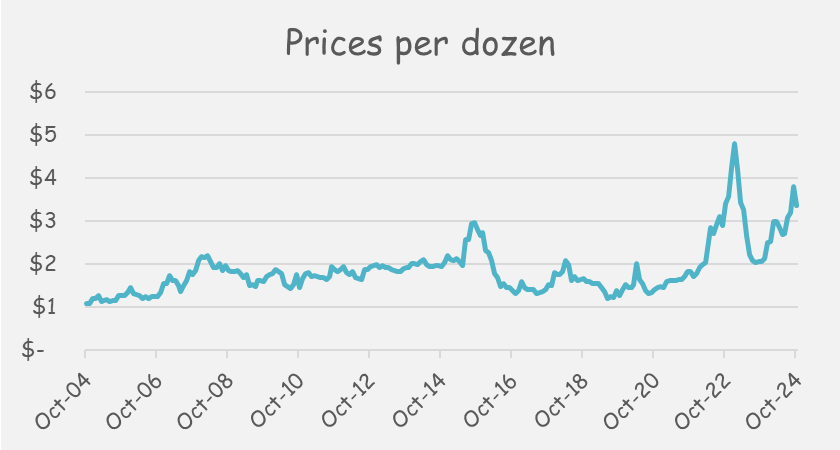

To understand the volatility of egg prices (per dozen), it is better to use the following chart, which shows the monthly prices over the last two decades.

Despite the volume of dozens sold being stable, it is impossible to forecast the revenue of the company over time, given the volatility of the prices. But this is just the start.

3.0 The direct costs

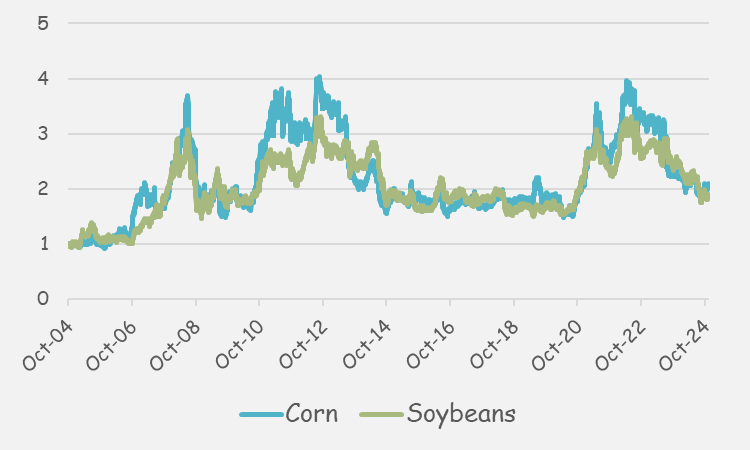

The largest direct cost relates to feed. The vast majority of the corn and soybeans are purchased from suppliers in the U.S. and there is quite some volatility.

*Prices are relative to October 2004

So the management isn’t in control of the costs, nor the revenue. That is a tough position to be in.

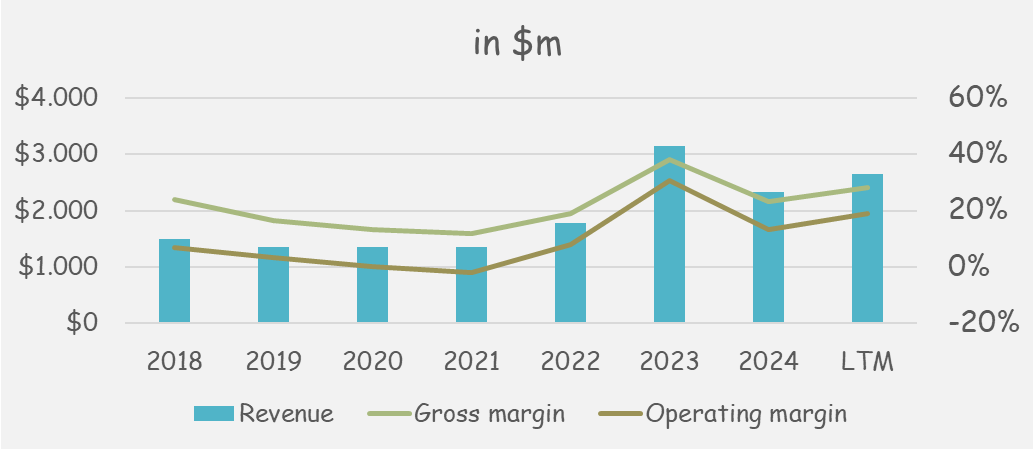

This is exactly why the financials look the way they do.

With a stable volume of dozens sold, the financials are all over the place. The gross margin has fluctuated between 12% to 38%.

The operating margin has fluctuated between -2% and 31%.

4.0 Now what?

So, what can the management do? Not much, other than being prepared for a bad year, as it is only a matter of time before that happens.

For that reason, the company has no debt.

In addition, its dividend policy is defined in relation to its profitability. The quarterly dividend payout is 1/3rd of its quarterly net income. This is definitely reasonable. Where does the remaining cash go to?

Acquisitions - There have been a total of 24 acquisitions, ranging from 160,000 to 7.5m layers.

Investment securities - Mostly U.S. Government and agency obligations, corporate bonds, and commercial paper.

I do think that the management does a good job, but the uncertainty scares away many investors.

5.0 Other important topics

5.1 Walmart

About 89% of the total revenue relates to sales to retail customers and 11% to food service providers.

Walmart (including Sam’s Club) is a major customer, accounting for 34% of its revenue. Although this might be perceived as a risk by many, I’d argue that is one of the biggest strengths the company has. Walmart has no alternative, as no competitor can quickly jump in to replace Cal-Maine.

5.2 The special shares

The company has two types of shares:

Common (trading on the Nasdaq exchange under the ticker symbol CALM 0.00%↑) - 44.2m shares outstanding

Class A - 4.8m shares outstanding, owned by an LLC

So, why are there two types of shares? Although both of them have the same rights in terms of dividends and liquidation, each class A shares is entitled to 10 votes.

This means the class A shareholders have 52% voting rights.

6.0 Valuation

So, how does one value a company of this kind when not only there are many pieces of the puzzle, but the pieces are changing?

Does a DCF make sense? Not really. There is no point attempting to forecast the next 5 or 10 years, when the next 2 are uncertain.

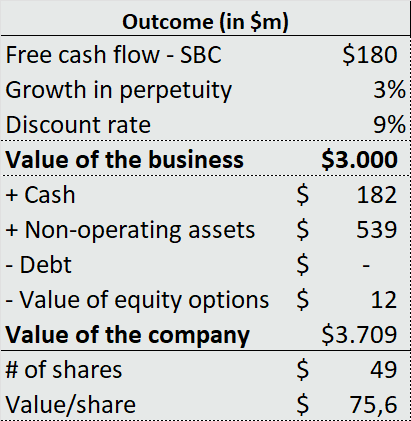

I’d argue that this is a company that could be treated like a bond, where the coupon is fluctuating, and a dividend discount model would be an appropriate way to value it. Except, instead of using the dividend, I’ll use FCF - SBC.

So, how to estimate the FCF? There will always be good and bad years in a company of this kind. So using the average of the last decade would be a good place to start.

Based on that input, the fair value of the company is $3.7 billion ($76/share). This is slightly lower than the current market cap of $4.6 billion ($91/share).

Note: If you use Google, you’ll notice a different market cap, as only the common shares are taken into its calculation.

So, anyone who is betting on Cal-Maine is ultimately betting that:

The egg market will remain stable, from a volume point of view - which is very likely

The future prices (eggs, corn, soybeans) will be slightly more favorable on average than the past prices - which is uncertain

Walmart will remain a key customer - which is likely

There will be no significant HPAI outbreak that will harm Cal-Maine - which is uncertain

The class A shareholders votes will be in the interest of all shareholders - given the past decisions, this is likely

The management will continue to run the company safely, without any significant debt position - which is likely

Based on the list above, there are two uncertainties, prices and HPAI outbreaks. Quite a lot to digest, for such a “simple” business. It’s only eggs, right?

I hope you enjoyed this post, feel free to share your thoughts.

Thanks for the analysis! I think a company like this one is best bought in the worst year, when they don't make any money. If the stock price reflects the poor results, then the risk is low as sooner or later things should normalize