Deep dive into Card Factory

A (not-so) dying company.

1.0 Introduction

In 1993, Dean Hoyle, along with his wife Janet, began selling cards from the back of their van at car boot sales and public open-air events.

Four years later, they opened their first shop in Wakefield.

Today, Card Factory has 1,090 locations and is the leading UK specialist retailer of greeting cards.

Now, when I heard about what the company does, I had two concerning questions:

Isn’t the card business a declining and dying one?

How is this still operating profitably?

By default, when these questions crossed my mind, I felt that this was a risky business, and there’s no point in doing any further research.

I believe many follow my thought process and form a similar perception.

However, this perception is not a fair representation of the company’s fundamentals.

In the short run, that doesn’t matter. The market is a voting machine. When market participants perceive a company as risky, it will come with a low multiple.

I believe the market participants are wrong.

Let’s get started.

2.0 Understanding Card Factory

The card business is responsible for approximately half of Card Factory's revenue, and, based on my estimate, accounts for most of its profits.

2.1 Vertical integration

The company is recognized as offering the best value for money in this product category. The reason for that is simple: they are vertically integrated, being in charge of:

Design (by acquiring design studios in 2006)

Manufacturing (by acquiring Printcraft in 2010)

Distribution

Route to market (online, retail, and partnerships)

Additionally, they collect a substantial amount of data, enabling them to make more informed decisions. It takes as little as 4 weeks to have a new design from concept to shelves.

This allows them to price their lowest cards at only 29p.

No competitor can match the value for money.

2.2 Dying business?

There are numerous market reports available, most of which indicate that the celebratory cards market size is flat or declining at a rate of 1% per year.

I wouldn’t classify this as a dying market per se. This is a product category that is deeply embedded in the UK’s culture.

If anything, if the market is slowly shrinking, it puts pressure on the smaller competitors that are not vertically integrated. If some of these competitors go out of business (or pivot to other products), Card Factory will gain a larger market share.

Despite the name being Card Factory, card-related revenue accounts for roughly 50% of the total revenue. It’s all because of the new management.

The rest? Gifts (picture frames, stuffed toys), party and celebration essentials, wrapping materials, and other seasonal merchandise.

3.0 The new management

Since March 2021, Darcy Willson-Rymer has been the CEO of the company. Given the timing (and the pandemic), I think we can all agree it was not an easy time to jump on board. Previously, he served as CEO of Costcutter Supermarkets Group for eight years, and before that, he held various roles in international businesses.

He’s making calculated bets.

If you want to hear his latest interview, here it is:

P.S. Interviews of this kind are primarily conducted with pre-agreed questions, so that the interviewee is presented in a favorable light. There were no tough questions asked.

Matthias Seeger became the company’s CFO in May 2023, after being the CFO of Costcutter Supermarkets Group for six years. To join a fellow C-level executive in another company, they must get along well. He brings in 30+ years of experience.

3.1 Change in Total Addressable Market (“TAM“)

The above is a slide from the Capital Market Strategy Update back in May 2023. Changing the focus from a £1.4 billion TAM to a £13.4 billion one in the UK, plus targeting international expansion, is a significant move.

In certain countries, the gift is what leads the purchase, and the card follows. In other countries, the journey is shifted. Card Factory aims to be the go-to place for both, starting with the card. After all, it’s literally in the company’s name.

This would significantly increase the average basket value.

Here are the steps taken to get there.

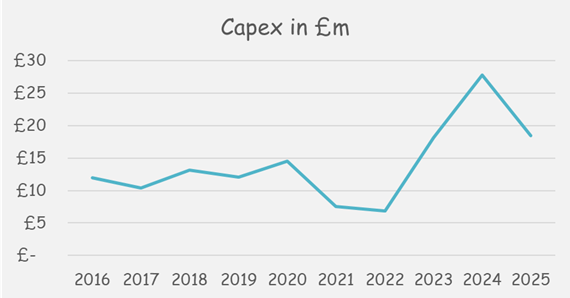

3.2 Reconfiguring stores

Allocating more store space to gifts is not an overnight activity, especially with over a thousand stores. Also, it’s not free.

Capital expenditure (“Capex”) was temporarily elevated compared to historical levels over the last few years.

3.3 Acquisitions (and international growth)

There were three acquisitions in a very short time:

SA Greetings (April 2023) - Wholesaler of greeting cards, gifts, and celebration essentials in South Africa (Purchased for £2.5 million - FY2025 sales £11.6m

Garlanna (September 2024) - Supplier of cards, gift wrap, and bags to independent retailers in Ireland (Purchased for £2.9m - FY2025 sales £3.8m)

Garven Holdings (December 2024) - Leader in design and wholesale of gifts and celebration essentials, with a primary focus on gift bags, wrap, and related accessories, located in Minnesota (Purchased for £19.6m - FY2025 sales £26.2m)

This is what I am referring to as calculated bets.

I don’t think Card Factory overpaid for any of these acquisitions; there’s some room for synergy, but most important of all, it allows them to figure out if they can go after the international markets with their know-how.

Best case - it works, and they move forward down this path. Worst case - it doesn’t, and they do not make decisions like this moving forward.

In FY 2022 (ending January 2022), only 2% of the revenue was international. In 2025, the international revenue was 6%.

3.4 Focus on online

This is a fairly standard task that most companies have had on their to-do list, even before the pandemic.

The only slight difference is that Card Factory can offer custom print-on-demand cards without any additional investment. They already have the capacity needed to serve this. I do think this is targeting more the younger population that appreciates the customization and is willing to pay a premium for it.

Of course, the goal is to have a gift attached to the card.

3.5 Partnerships

Last but not least, there are partnerships in place, with Aldi in the UK & Ireland, and The Reject Shop in Australia. This was non-existent before 2022, and now it generates £22m in revenue, 30% higher than the previous year, representing 4% of the total revenue.

4.0 Historical Financial Information

The number of stores has been slowly growing and increased by 34% over the last decade.

At the same time, 99% of all locations are profitable, with an average payback time of less than two years.

Not bad for a dying company.

Over the last decade, the revenue has increased from £382m to £543m (average growth rate of 8%).

Although the gross margin is improving, the operating margin is the elephant in the room that concerns many.

Prior to the pandemic, it was above 20%. Now, it’s stable at around 15%.

In absolute terms, the operating profit is flat.

There’s another way to look at this, which is per store.

This brings another angle. Almost all of the revenue growth is from the increase in the number of stores.

The operating profitability has significantly decreased compared to 2016.

Why? Card Factory is not yet the go-to place for non-card items. Building and expanding a business line requires significant investment, as well as an increase in operating expenses.

The positive aspect of the story that I believe is often overlooked is the growth in operating profit per store over the past few years. I think this trend will continue. Although one can argue that this is a relatively simple business, focusing on so many areas (partnerships, online, acquisitions, international growth) brings a lot of complexity.

Additionally, the cost increase hasn’t been fully passed on to the end customers.

Over the last years, the FCF has averaged £33m. Once capex is normalized, it should increase to at least £40m. This is excluding any price increases or cost rationalization.

A fun fact: During the pandemic lows, the market cap was ~£110m.

5.0 Valuation

Here’s my DCF model. I’m assuming:

Slight revenue growth, primarily driven by inflation;

Stable operating margins; and

No significant surprise coming out of the international expansion

Based on it, the company’s fair value is ~£411m (£1.18 per share), ~30% higher than the current price, offering an IRR of ~14%.

5.1 Capital allocation

This is the last piece of the puzzle that I find relevant, and it comprises four elements:

The management has reiterated multiple times that they want to maintain a strong balance sheet. This means it is unlikely to expect a significant debt burden in the future.

The second element is investing in the future of the business, where they see fit. So far, they’ve done this by reconfiguring the stores and acquiring smaller companies.

Return cash to shareholders via dividends in a progressive way. The current dividend yield is ~5.3%, but the payout ratio is only 35% of the earnings. If all the profits were distributed as dividends, the dividend yield would be very close to what I expect the IRR to be in the long run. I believe this will change in the coming period, and more of the cash generated will be returned, bringing us to the last element.

If there’s excess cash, return it to the shareholders. All options are on the table. There have been no share buybacks, but I would not be surprised if that changes.

5.2 Risks

There are two key risks, and they’re not related to their card business in the UK.

Limited international experience - Although the management team has international experience, this is a different business that they haven’t cracked (yet).

Product mix transition - Entering a category where the company doesn’t have the same dominance or sourcing advantage as in cards could backfire.

The perception that the market participants have about Card Factory, combined with these two risks, is why it’s trading at a low valuation.

If you found this deep dive valuable, consider sharing it with someone who would, too. Your support helps grow The Finance Corner and brings more deep dives like this to your inbox.