Deep dive into Celsius ($CELH)

Is it becoming Monster Beverage 2.0?

For those who prefer to watch, here’s the post in video format:

For those of you who prefer to read, well, here’s the written version:

Celsius Holdings CELH 0.00%↑ is riding on top of the memories of the exceptional returns of Monster Beverage MNST 0.00%↑ .

The question is - is this comparison fair? Is Celsius becoming Monster Beverage 2.0? To answer this question, I’ll walk you through plenty of information that I think anyone interested in the company should be aware of.

1.0 The Bull Case

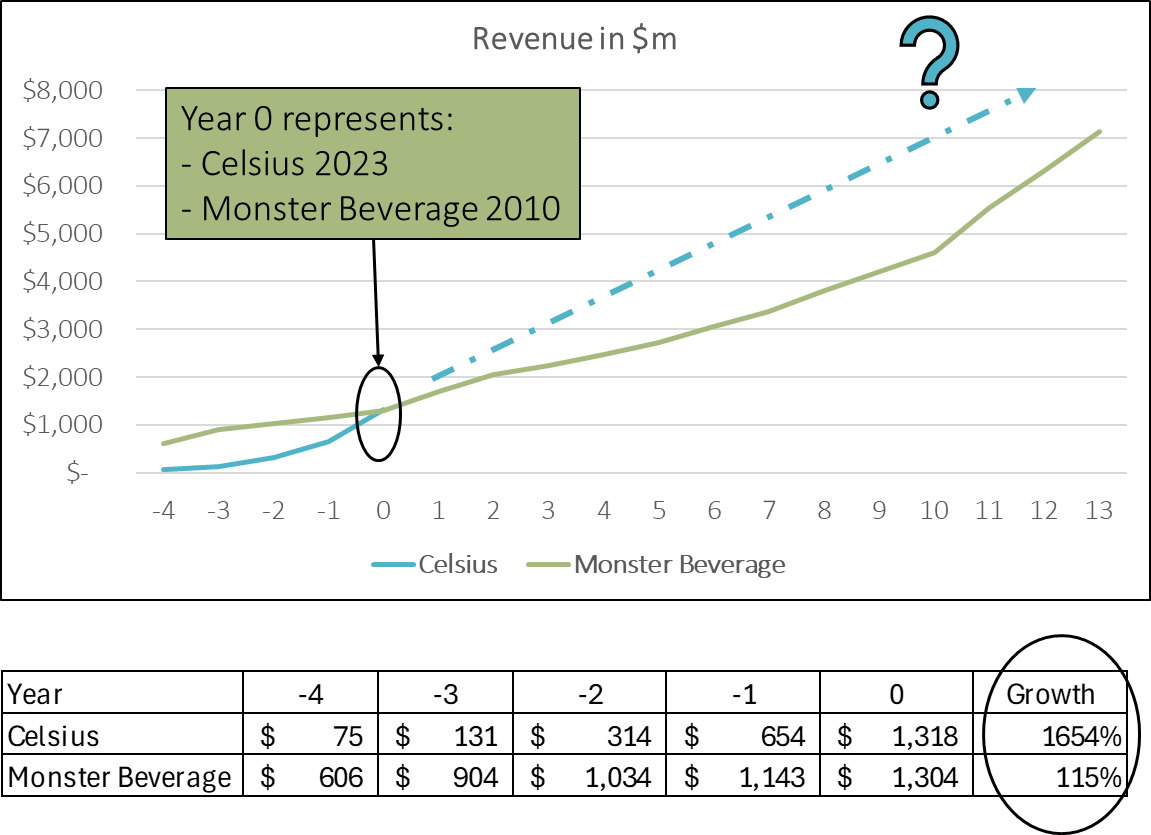

In 2023, Celsius had revenue comparable to Monster Beverage back in 2010. However, it was growing at a much faster pace.

This brings a lot of excitement and the main question is - Will the revenue growth continue in the next decades? Since 2010, the share price of Monster Beverage is up over 1,000% (vs. 350% for the S&P500).

2.0 Pepsi - the key stakeholder

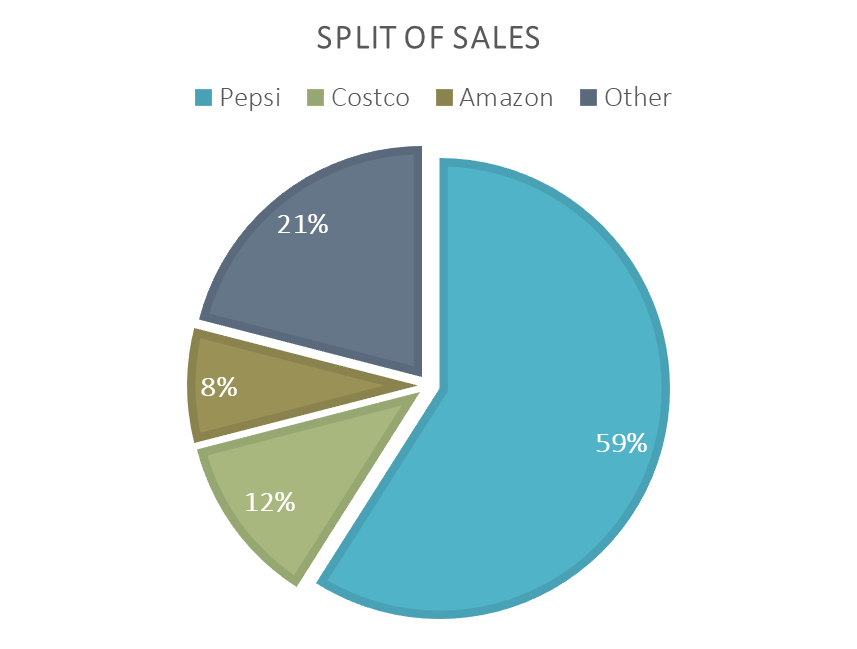

Before we dive into all the financial fun stuff, it is important to introduce Pepsi, I’ll argue, the most important stakeholder. It is not only the exclusive distributor but also owns part of Celsius through so-called mezzanine financing (a hybrid of debt and equity). The ownership is slightly less than 10% and it is enough to align the incentives. This also opens the door to a potential acquisition in the future.

Pepsi accounts for almost 60% of all the Celsius sales. You might wonder, wait a second, isn’t Celsius selling products to the final customers? Ultimately, yes. The customers’ definition of Celsius is Distributors, Brick-and-mortar outlets, club stores, and health-focused locations.

Distribution is key in a business of this kind. Ideally, you’d like to partner with someone who has a large reach and can quickly distribute the product to the final customer. Pepsi is a great match. However, given its size, it has a lot of negotiation leverage, especially when it comes to pricing.

3.0 The bull case continued

For Celsius to follow in the footsteps of Monster Beverage, it needs to grow, a lot. In my opinion, there are 3 ways for that to happen:

Expand into new markets

North America accounts for 96% of all the revenue that Celsius brings. For comparison, this is only 65% for Monster Beverage.

The good news is: There is a lot of room for expansion, and the company is already working on this. During 2024, sales are expected to begin in Canada, the UK, Ireland, Australia, New Zealand, and France.

Steal market share from its competitors (in existing markets)

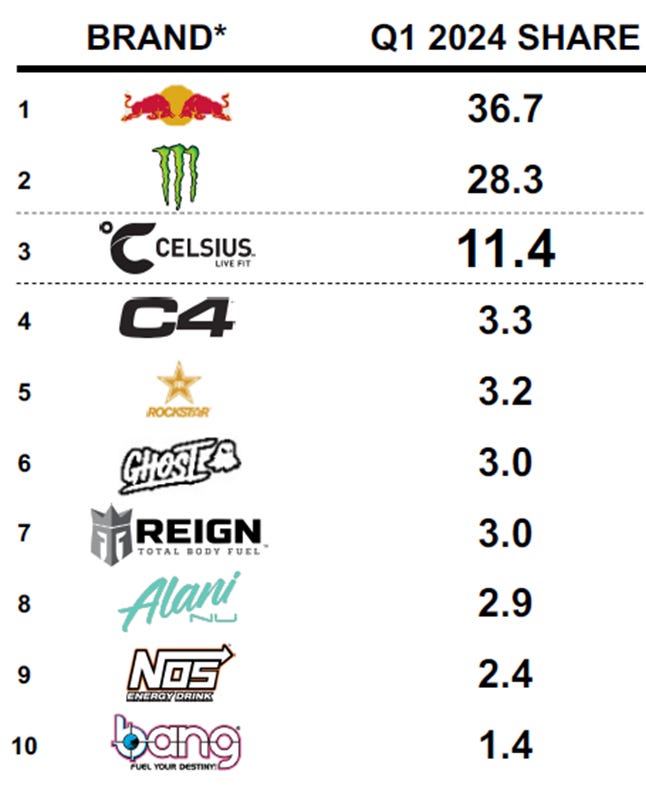

Based on the Q1 data, Celsius holds the #3 spot in the U.S. energy drinks market with a market share of 11.4%. This is definitely impressive growth. However, the latest data show that its market share has decreased to 10.5% - which indicates that the upper limit is being tested. In addition, on June 11, Celsius’ management shared that Pepsi would reduce inventories of the energy drink by another $20-$30 million in the second quarter, which followed a $45 million reduction in the first quarter. This could be another indication that the supply outweighs demand and the hypergrowth days might be over.

Let’s not forget, this is a tough landscape to compete with. Red Bull, Monster Beverage, and even Pepsi are established players.

Introduce new products (expand into new verticals)

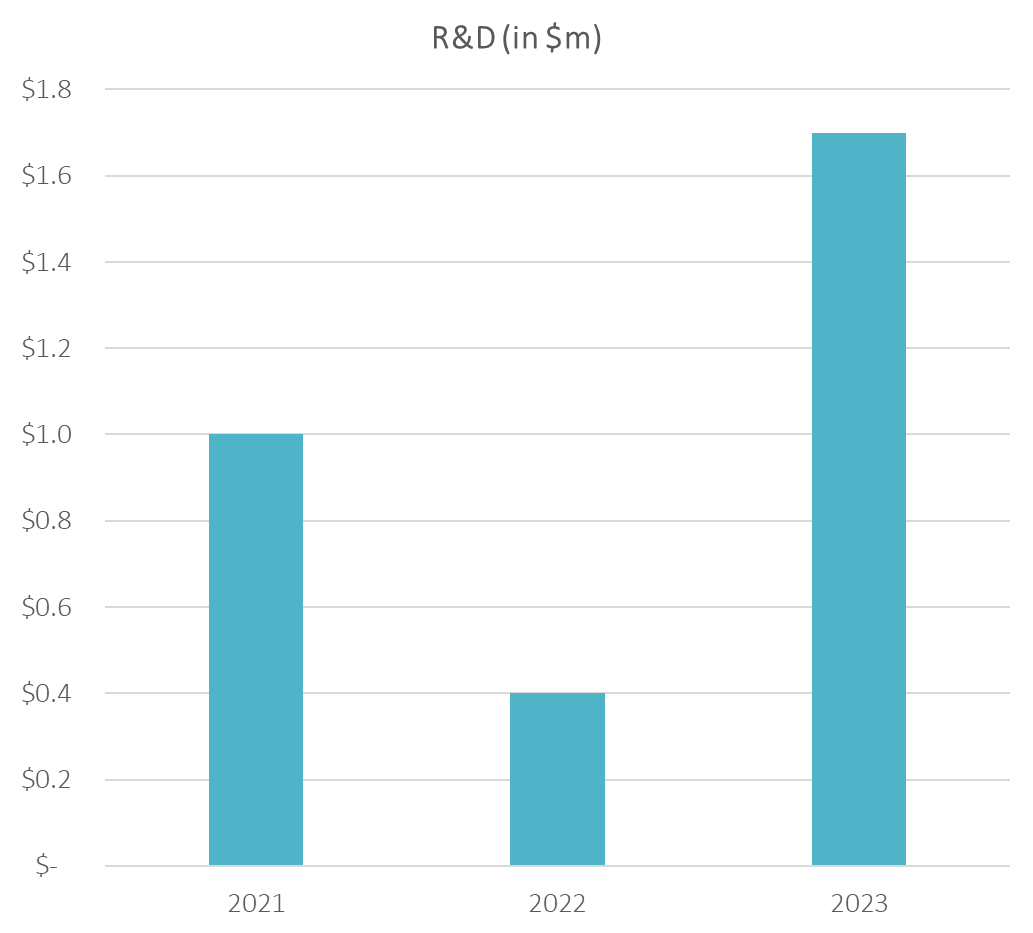

Lastly, for a company to innovate, it needs to invest in Research and Development.

Unfortunately, there isn’t much of that happening. The R&D expense is below 0.1% of revenue, so I don’t have high expectations for new products or verticals (such as protein bars) unless it comes through an acquisition.

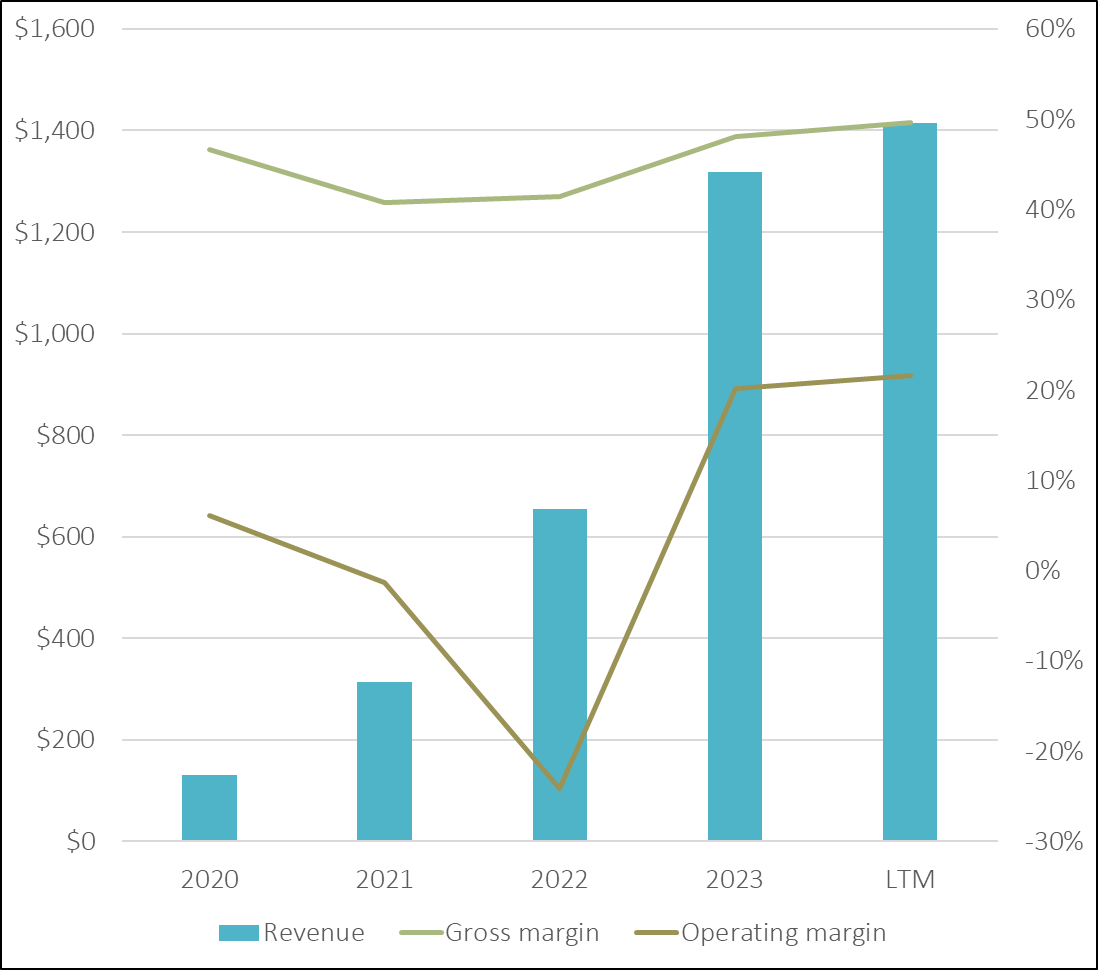

4.0 The historical financial performance

The company is in charge of development and marketing, while the manufacturing is outsourced. This, combined with Pepsi’s distribution, allowed the company to grow at this incredible pace, without having to invest too much.

For comparison, Monster Beverage has:

55% gross margin

29% operating margin

It is quite clear that Celsius isn’t at the same level.

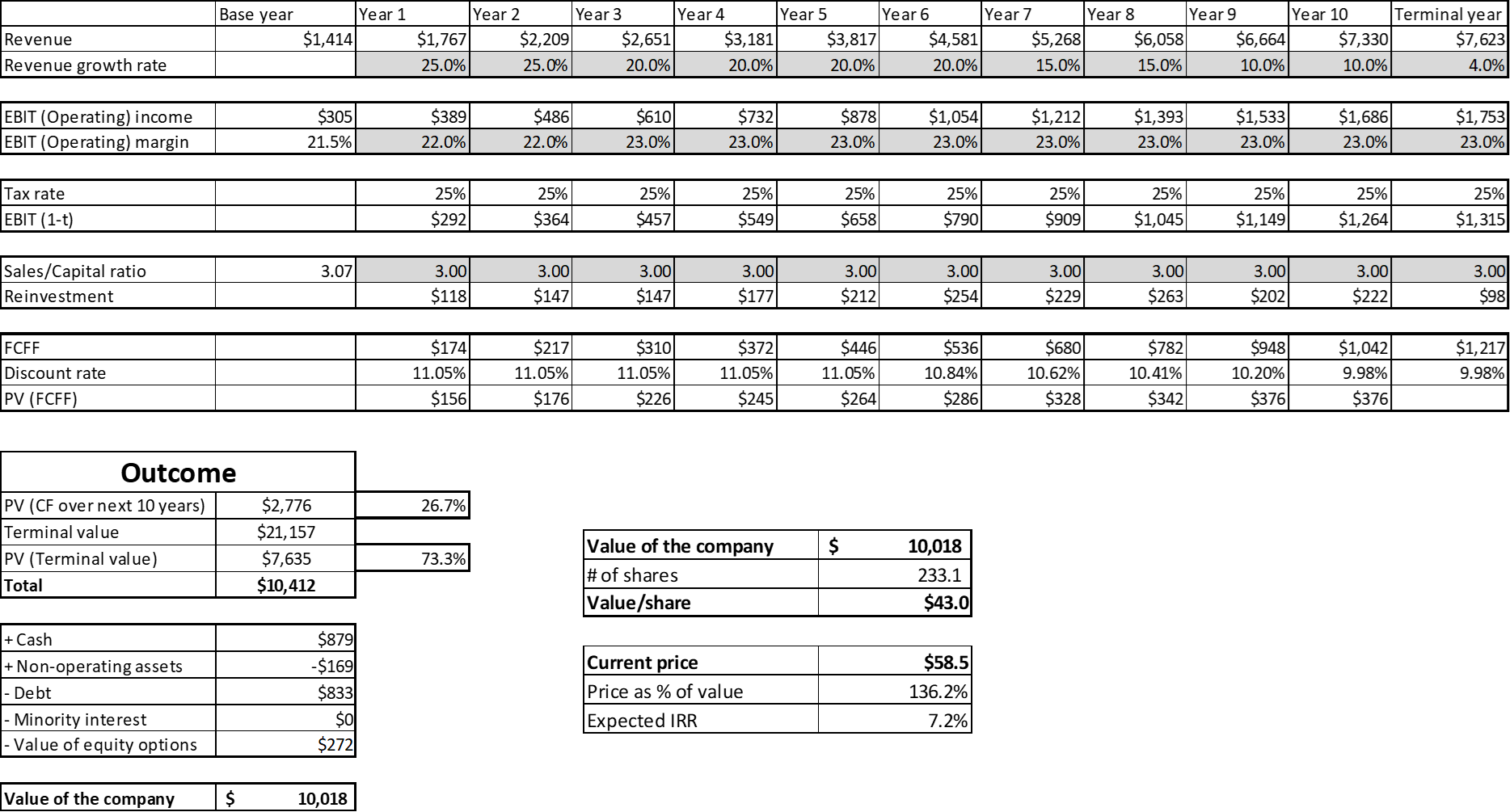

5.0 Valuation

Based on my assumptions, the fair value of the company is roughly $10 billion ($43/share), slightly below today’s share price. The two key assumptions to focus on are:

Revenue growth

Operating margin

Here’s how the valuation (per share) changes if you have different assumptions than mine:

Currently, the market price is $58.5, which implies high expected growth for an extended period of time. If the growth rate decreases below 25%, I do expect a significant market reaction.

However, if you believe Celsius is the next Monster Beverage, will grow at the same pace for an extended period of time, and will reach the 29% operating margin, then the company is undervalued.

Should the price drop below $40, I might revisit the company and see if my thesis is still intact. Until then, I’m happy to follow the company from the sidelines.

I hope you enjoyed this post, feel free to share your thoughts.