Deep dive into Intuit

The most hated stock in the S&P500

1.0 Introduction

The fear of AI has reached Intuit.

The share price chart below looks terrifying.

The first time I looked into Intuit was in September 2022. Back then, it was a $127b company with ~$13b in revenue. My estimated fair value at the time was roughly half of the market cap. I couldn’t justify the premium.

Today, the revenue is $21b (+60%), while its market cap is $81b (-36%). Time to look into it, for the second time.

As I’m writing this, Intuit is the worst-performing company in the S&P500 in 2026 (down 56%).

Disclosure: I have no position in Intuit.

2.0 What is Intuit offering?

In 1983, Scott Cook (one of the two co-founders) watched his wife sit at the kitchen table, struggling to balance the family checkbook. He was aware of the power of personal computers, so together with Tom Proulx, they created Quicken, a software to manage personal finances.

Today, there’s QuickBooks (bookkeeping software for small businesses), Mailchimp (sends marketing e-mails), Credit Karma (shows credit score, for free), TurboTax (files taxes), and the list goes on.

Millions of individuals (and SMBs) use Intuit’s tools to:

Get customers and communicate (Mailchimp)

Pay and get paid (Credit/debit card, Apple Pay, instant deposit, payment dispute protection, QuickBooks checking, online payments)

Get capital (either via bank partner or QuickBooks Capital marketplace)

Manage employees (payroll, tax payments and filings, health insurance, 401(k) plans)

Advice (QuickBooks Live, QuickBooks Pro Advisor)

Compliance (QuickBooks Online, Intuit Enterprise Suite, etc)

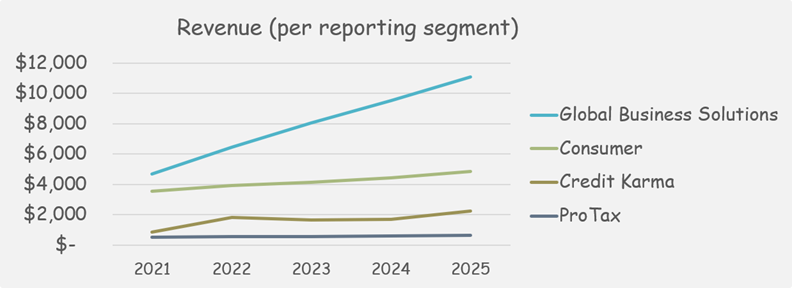

The above bullet list is included in the Global Business Solutions and Consumer segments.

There is also Credit Karma. It offers consumers access to credit scores, monitoring, and financial tools, and earns revenue from financial institutions when consumers take action on recommended products.

Lastly, ProTax is the professional accountant segment (Lacerte, proSeries, proConnect). If an accountant learns how to use these tools and builds workflows around them, the chance of switching to another solution is very low.

The chart above doesn’t show a business that is being disrupted, and I believe there’s an easy answer to that.

The market has decided that if an LLM can answer tax questions, then nobody needs TurboTax, and if an AI agent can do bookkeeping, then there’s no need for QuickBooks.

I think the opposite is true: Intuit is benefiting greatly from AI.

3.0 Why is Intuit not getting disrupted?

There are 5 points worth addressing:

It’s an affordable ecosystem. The offering is huge and not vibe-coding worthy. Here’s why. An accounting software to log data can be vibe-coded in a weekend (Trust me, I’ve done this). But then, what about feeding bank transactions into it? What about reconciling all transactions? What about having access to your mobile phone? What about tax filings? What about payroll? All of those questions (and there are a lot more) require more development time. But it doesn’t stop there. Any API change requires additional debugging time. Any changes in the accounting/tax rules require more development time. Ultimately, those who attempt to do this will pay more and get less. Doesn’t sound like the best idea.

Accounting and tax services, in general, have a high retention rate. Migrating data to another software is a hassle that nobody looks forward to, and a slightly cheaper alternative is not enough to make this call.

QuickBooks has an acquisition engine. Its plans start at below $3/month for 6 months, which is enough to get data in their software to make you not want to move away.

AI helps. Agents are real. There’s nobody better positioned than Intuit to take advantage of it. They have valuable data to train on and help the users.

Accountability is not optional. Whatever the activity is, someone has to be accountable for it, as eventually, things go wrong. This is best seen in the growth of TurboTax Live revenue by 47% in FY2025, to $2 billion.

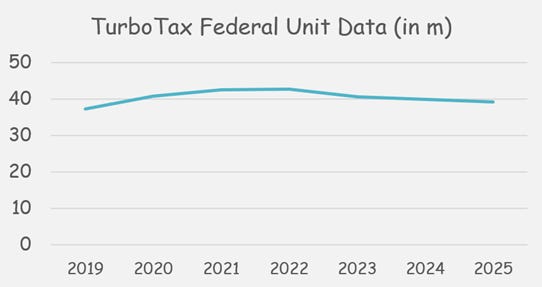

The only area where a decline is visible is the TurboTax Federal Unit Data:

In 2023 (the first year when ChatGPT was available), the filings via TurboTax decreased by 5%. They continued to decrease by <2% in 2024 and 2025 as well, and are projected to decrease by 1% in 2026.

That’s 9% (compounded) decrease from the 2022 top, which was more than compensated by price increases. The bear argument is: a model can be trained on the 56,000 pages of tax code, which continues to evolve, with state-level complexity on top.

But, if that is the way to go, isn’t Intuit best positioned for that? It has a significant data advantage, as it has hundreds of millions of tax filings over the years, and the ecosystem to connect with the top tax specialists.

4.0 Historical Financial Data

The revenue is there. The profitability is there.

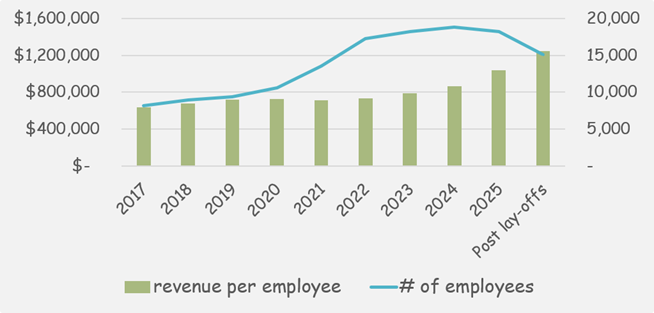

The chart below shows the power of high-retention products.

Regardless of the interest rates, COVID, and unemployment, the demand is there. The only thing that changes is the productivity of the employees.

In May, the company announced its plans to lay off 17% of its workforce in the next 6 months, and invest the savings in “big bets“ as it makes AI a centerpiece of its business. In this period, there will be ~$320m additional costs, which is 5% of its operating profit.

Fewer employees, higher revenue. That’s the impact of AI.

The revenue per employee has increased from $633k in 2017 to over $1.2m (estimated, post lay-offs).

5.0 Capital allocation

Intuit is, no doubt, a cash-generating machine.

In the last year, its free cash flow (adjusted for share-based compensation) was ~$5.5 billion, which is a 7.5% FCF yield on a company with an enterprise value of $73 billion, that is still growing.

But the management’s decision to allocate this excess cash can create or destroy the company’s value. There were some really, really bad decisions.

Starting with acquisitions.

5.1 The Acquisitions

Intuit wasn’t known for making huge acquisitions, and that changed.

In December 2020, Credit Karma was acquired for $8.1b. Today, it brings in ~$2.6b in revenue and about $1b in operating profit. Given that more than half of the payment was in equity (which was overvalued at the time), this was a good decision.

Then comes the bad one. Mailchimp was acquired in November 2021 for $12b (of which $5.7b was cash) with ~$800m in revenue. The synergies were significantly overestimated, and because Mailchimp is in the largest segment, its underperformance is masked by QuickBooks’ outperformance. In hindsight, not the best choice.

To illustrate how poorly Mailchimp aged, the management is still breaking out growth “excluding Mailchimp“ in every release, and the excluded number is always better. Here’s the extract from the last quarterly release: ‘

“Increased Global Business Solutions revenue to $3.3 billion, up 15 percent; grew Online Ecosystem revenue to $2.5 billion, up 19 percent. Excluding Mailchimp, Global Business Solutions revenue grew 17 percent, and Online Ecosystem revenue grew 22 percent.“

If a company keeps showing a metric without the acquisition, the acquisition is not going well.

5.2 Buybacks & Dividends

Based on my estimate, the company was overvalued until the recent price drop. During the overvalued phase, the company kept buying back shares.

Over the last 5 years, more than half of the free cash flow was used to buy back shares, and I have no choice but to label that as a bad capital allocation choice.

Lastly, about 20% of free cash flow was returned as dividends. I don’t mind this part at all.

6.0 Valuation

Is there uncertainty? Yes, always. That makes valuing companies fun.

Writing down what I expect to happen is a great way to test my ability to assess my understanding of a company and its trajectory.

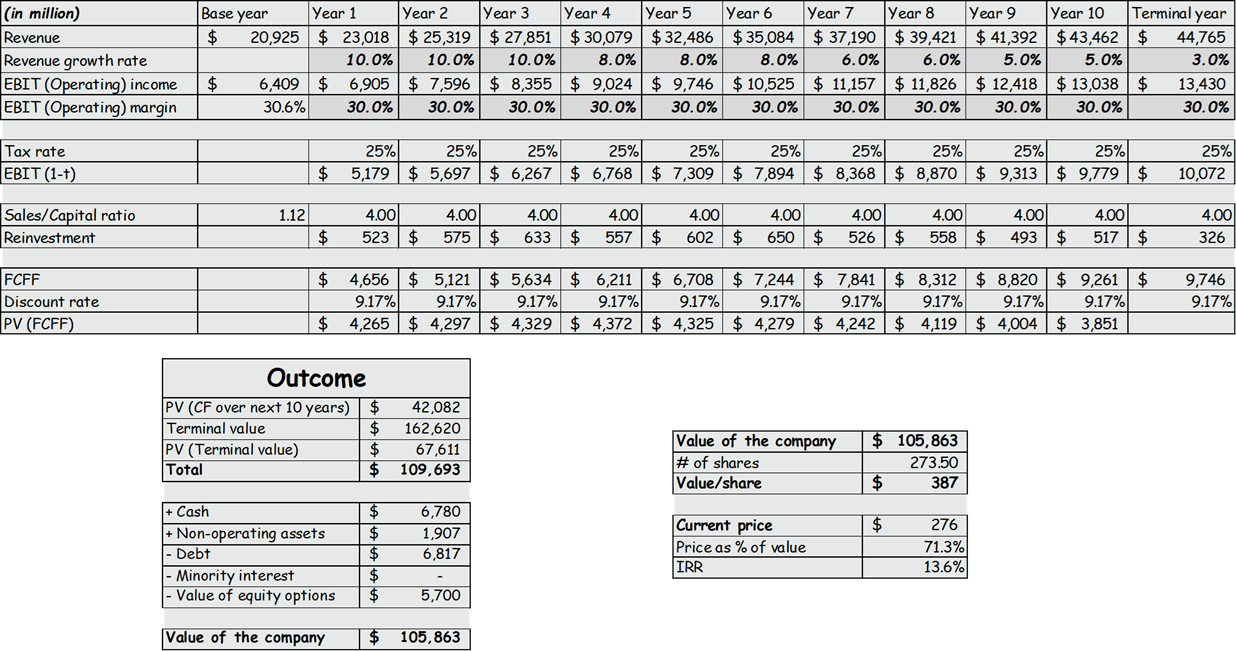

Overall, I am bullish on Intuit, and here are the assumptions behind my optimism:

I do think the TurboTax units will stabilize and tax-filing related revenue will continue to grow, driven by TurboTax Live.

At the current price, the company is undervalued, so the buybacks are creating value for the shareholders.

AI will allow QuickBooks to develop more features (and Intuit Enterprise Suite) and go after significantly bigger clients, where the price is significantly higher.

AI will create more small companies over time, which will end up paying for QuickBooks.

Based on the above assumptions, the fair value is $106 billion ($387/share), around 40% higher than the current price. It can even be argued that the above model is conservative, as I’ve kept the operating margin roughly the same.

Note - In my calculations, I’ve ignored the amortization of acquired intangibles, as it has no cash impact.

7.0 Risks

The risk everyone talks about is AI commoditizing DIY tax filing. I don’t think this is what puts Intuit out of business.

The second risk is the government. IRS launched its own Direct File pilot in 2024, and while the current administration has walked away from it, the underlying idea remains. The US is one of the few rich countries where citizens pay to file taxes. I don’t take this risk seriously, mostly because governments are terrible at creating value in this form, and Intuit’s solution will always be superior.

Third, the legal track record isn’t clean. There were fines/settlements in the past over “free'“ TurboTax marketing and an FTC order banning deceptive advertising. Right now, there are three securities-fraud investigations into how the 2026 pricing strategy was disclosed.

Lastly, when there are loans, there are risks. Intuit has a lot of data on its customers, but that doesn’t mean the decisions will always be perfect. As the loan balance grows, the risk exposure in case of a recession can be troubling.

So, why haven’t I invested?

When the free cash flow is so significant, there is pressure on the management to put it to use. Given their past decisions, specifically the Mailchimp acquisition and buying back shares, I don’t feel too comfortable with their capital allocation decisions.

This is NOT investment advice. Everything above is for entertainment, informational, and educational purposes. Do your own due diligence.

I enjoyed this, I'm also looking at Intuit at the moment. My fair value is more conservative than yours, but I also think the 60% drop this year has brought it into range and I have opened a small position. I think most would agree with the SBC risk, which I think will become more substantial in the future for options being issued at current prices, and MailChimp, but even including MailChimp, the growth rate is sufficient for me to invest at current prices. I also note that the MailChimp acquisition hasn't been impaired (yet).