Deep dive into Kraft Heinz ($KHC)

A value opportunity backed by Warren Buffett

1.0 Introduction

Warren Buffett, the legendary investor, is a human being. This deep dive outlines one of his biggest mistakes.

In March of 2015, Berkshire Hathaway and the Brazilian investment firm 3G Capital engineered a merger between Heinz and Kraft Foods Group.

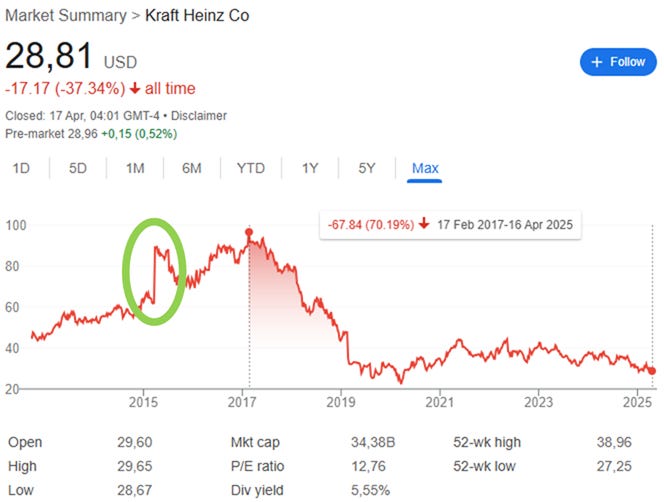

The share price was up more than 35% on this news (the green bubble below).

Fast forward to today, the share price has gone down significantly.

But let’s start from the very beginning.

2.0 Kraft Heinz

2.1 H.J. Heinz

H.J. Heinz Company was founded in 1869 by Henry John Heinz, and the first product was grated horseradish, sold in clear glass bottles to showcase purity and quality. This was a huge difference from the competitors, who often used colored bottles to hide impurities.

Next, the company expanded into ketchup, launching its iconic Heinz Tomato Ketchup in 1876.

Its slogan, “57 Varieties,” was introduced in 1896 despite the company offering way more products. So, why 57? Because Heinz liked how it sounded.

In the 20th century, it expanded internationally and introduced products like baked beans, vinegar, pickles, mustard, and canned soups.

2.2 Kraft Foods Group

In 1903, James L. Kraft, a Canadian immigrant, started selling cheese door-to-door. The company name was J.L. Kraft & Bros. Company.

In 1916, the company revolutionized the food industry by patenting pasteurized processed cheese. This extended the cheese's shelf life and helped supply U.S. soldiers during World War I.

In the 1920s, the company was already the leading cheese producer in the U.S. and acquired Philadelphia Cream Cheese in 1928.

In 1930, it merged with National Dairy Products Corporation, forming Kraft Foods.

In World War II, Kraft supplied the U.S. military with processed cheese and powdered cheese for macaroni.

2.3 The Merger

The merged company became one of the largest food and beverage manufacturers, owning numerous strong brands.

Berkshire is known for investing in companies of this kind. If start-ups have the highest chance of failure, companies that have been around for decades have the lowest chance (right?).

Here are the top 8 holdings in the Berkshire Hathaway portfolio:

Apple (Founded in 1976);

AXP (Founded in 1850);

Bank of America (Founded in 1904);

Coca-Cola (Founded in 1892);

Chevron (Founded in 1879);

Occidental Petroleum (Founded in 1920);

Moody’s Corp (Founded in 1909);

Kraft Heinz (merged in 2015, Heinz founded in 1869, Kraft Foods in 1923);

Berkshire had shares in Heinz before the merger, and Buffett was optimistic about this deal. Both companies have strong brands but struggled with slow growth during the merger.

The idea was simple: merge the two and drive profitability through cost-cutting and efficiencies.

Warren Buffett said, “I’m delighted to play a part in bringing these two winning companies and their iconic brands together.”

Today, Berkshire owns ~27% of the company (although 3G Capital sold its shares in 2023, realizing a loss).

Did Buffett make a mistake? Why is Berkshire still holding Kraft Heinz in its portfolio?

3.0 The post-merger challenges

The merged company started its journey with ~$30 billion in debt, which was more than its annual revenue. At the same time, the dividends paid out were close to 100% of the free cash flow.

So the only way to service and reduce the debt was to have real cost-cutting savings.

However, the cost-cutting led to underinvestment in innovation, marketing, and supply chain, which stagnated key brands such as Oscar Mayer and Kraft.

In addition to that, creating synergies by merging two large companies sounds excellent in theory, and is often overestimated.

By the end of 2018, Kraft Heinz had $2 billion more in debt than in 2016.

Warren Buffett admitted that the payment for Kraft Foods (as part of the merger) was too high. Here’s an interview with him back in 2019.

4.0 The Drastic Measures

The capital allocation wasn’t sustainable, and a key decision was to cut the dividend payment and use that cash to pay down debt.

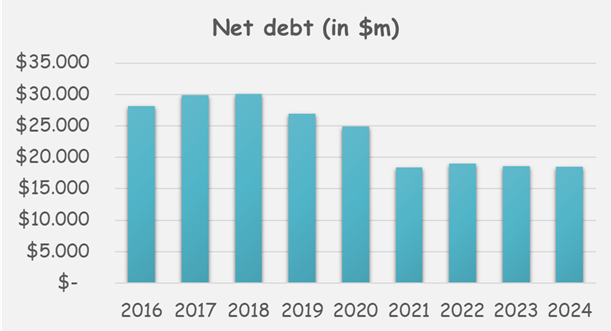

Between 2016 and 2024, the net debt was reduced by ~$10 billion, which sounds impressive.

However, the chart doesn’t tell the whole story. Between 2019 and 2021, when the debt was significantly reduced, Kraft Heinz got ~$7 billion for selling its Natural Cheese Business to Lactalis and its nuts business to Hormel.

5.0 The Kraft Heinz today

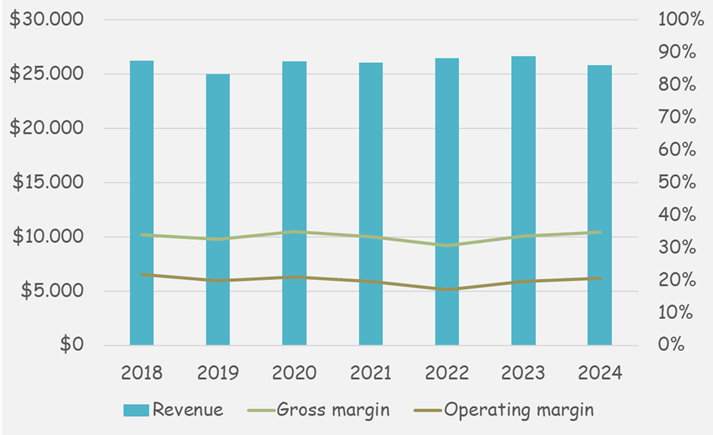

The chart below outlines the revenue and margins of Kraft Heinz (excluding the impairments mentioned earlier).

Despite the divestments, the revenue and margins remained stable. It is a true cash cow, generating ~$3 billion annual free cash flow.

So, where does the $3 billion go?

The reduced dividend payout takes ~$2 billion.

The remaining $1 billion? Last year, it was used to buyback shares, reducing the share count by 1.5%.

With ~27% ownership, I believe Buffett is behind the capital allocation strategy of Kraft Heinz. The decision to buy back shares is an indication that he finds the company undervalued today.

6.0 The Competitive Landscape

This company operates in a boring industry with little to no fundamental innovation, so it appeals to dividend and risk-averse investors.

Its key competitors are giants like Nestle, Unilever, General Mills, Mondelez International, and Conagra Brands.

This is an industry that has a high barrier to entry. For a new company to be successful, it requires:

Significant initial investment (R&D and manufacturing facilities);

Securing access to distribution, particularly prime shelf space in major supermarkets;

Higher marketing to create awareness in addition to the ongoing marketing; and

High market adoption, so that economies of scale are available.

None of the above is easy.

As the world focuses more on tech and the next big thing, old-school companies will become the most difficult to disrupt.

7.0 Valuation

So, how much is Kraft Heinz worth?

Below is my DCF model, which is based on 2% annual revenue growth & an operating margin of 20%, slightly below the historical average.

Based on my assumptions, the company is worth ~$40 billion ($33/share), slightly higher than its current market cap of $34.4 billion ($28.8/share).

Kraft Heinz is the cheapest it has been in a long time and slightly undervalued, which supports the decision to buyback shares.

At the same time, this is a stable company with low volatility when it comes to its fundamentals. Low risk goes hand in hand with low return, which is why the discount rate is at 7.5%.

This might not be attractive for risk-seekers with long time horizons, but I’ll argue it is interesting for risk-averse investors who focus on dividends.

If you found this deep dive valuable, consider sharing it with someone who would too. Your support helps grow The Finance Corner and brings more deep dives like this to your inbox.