Deep dive into Lululemon ($LULU)

Outsmarting Nike and Adidas

1.0 Introduction

At first glance, Lululemon LULU 0.00%↑ seems like an apparel company that somehow continues to do well, despite selling overpriced products.

However, there’s a lot more than that. I’ll argue it should be a case study in every business school, as it continues to outsmart giants like Nike and Adidas.

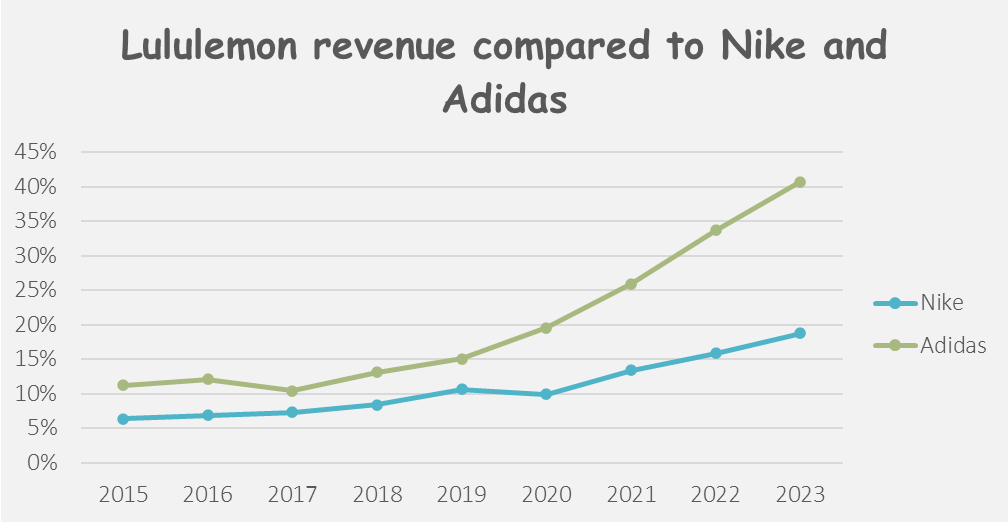

Lululemon has been growing its revenue at an average rate above 20% annually for a decade, significantly higher than Nike’s 6%, and the disappointing 3% of Adidas.

Not only is Lululemon increasing its market share, but it is significantly more profitable than its competitors.

How is this possible?

2.0 Its secret formula - Ignoring the rules

The big companies out there spend millions on celebrity endorsements. This approach brings exposure quickly but is very expensive.

Nike has Michael Jordan, Tiger Woods, and Rafael Nadal.

Adidas has Lionel Messi, David Beckham, and James Harden.

Under Armour has Dwayne Johnson, Tom Brady, and Steph Curry.

What about Lululemon? Well, there’s no celebrity.

Lululemon took a different approach. Instead of paying millions to celebrities, it partners with micro-influencers, yoga teachers, and fitness instructors, who are largely unknown. These people live more ordinary lives and one can easily connect with them.

They’re known as “brand ambassadors“ and they get to host Lululemon events. In return for promoting the brand, they get:

Free Lululemon apparel;

Priority access to new products; and

Featured on Lululemon’s social media and website, which generates more traffic for them and helps them build/grow their business and audience.

Not only is it a much cheaper way for Lululemon, but it also allows for thousands of communities to be formed, that are likely to stay together. The outcome is clear: Stronger, deeper, emotional relationships are formed, that are not purely transactional.

This is the company’s MOAT - Creating a cult-like following.

In addition, there are larger outdoor events, 10k runs, sweat games, etc.

3.0 Too Expensive Products - So What?

The company’s products are significantly more expensive than the competition. They capitalized on the increase in demand for athletic, stylish, yet versatile clothing that eventually became known as “athleisure“.

There is no doubt that the products come with exceptional quality, thanks to a combination of innovative fabrics and superior design. In addition, there is free hemming that comes with a Lululemon membership. This service ensures that the product purchased fits the customer.

Combining all of this, with the community aspect above, allows the company to charge a premium price for its products.

The two main competitors in the U.S. are now Alo Yoga and Vuori and there are plenty of copycats. There is even a #lululemondupe hashtag on TikTok with over 9,000 posts. This is being perceived as the biggest risk, yet, the company continues to grow and deliver.

Is the demand for its products going to decrease?

History has taught us that there will be demand for premium brands, especially in the fashion industry. From Dior and Louis Vuitton to Rolex and Balenciaga, all of them face copycats. Yet, they are still around and doing well.

For that reason, I do believe Lululemon will continue to grow in the years to come, especially given the fact that the company’s international expansion has just started (~80% of the revenue comes from the Americas).

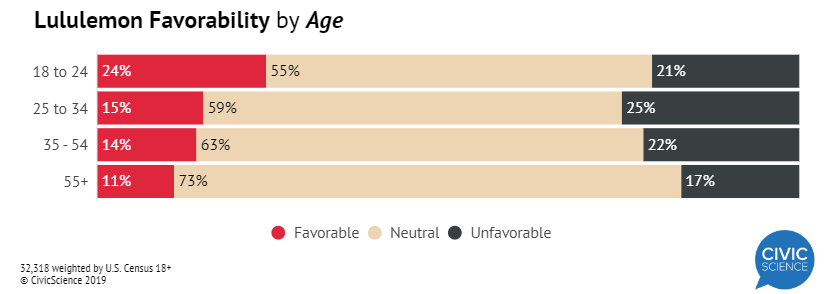

In addition, the younger generations have a more favorable view of Lululemon. The company will only benefit from this trend over time.

4.0 Historical Financial Performance

As mentioned at the very beginning, the company’s margins are significantly above its competitors. There are two main reasons for that:

Advertising - which was already covered above; and

Selling directly to consumers - Over 90% of all the sales are online, or through the company-operated stores. This means in most cases, there is no 3rd party in between collecting a fee.

As the company is profitable and generates lots of free cash flow, it is worth having a look at the other side of the equation. Where does the cash go?

Capex - In order to grow, the company has to reinvest in opening new stores.

Share buybacks - The number of shares outstanding is down ~10% over the last decade.

5.0 Past Mistakes

Before I move to the topic of valuation, two management decisions can be labeled as mistakes:

In June 2020, Lululemon acquired Mirror for ~$500m. Fast forward to Q4-2022, and the business has now almost been entirely written off. The in-house fitness company that created an interactive workout platform featuring live and on-demand classes did not do as well as expected post the pandemic.

The share price of the company went up significantly on a few occasions, and the management decided to continue buying back shares. I do think above a certain point, share buybacks destroy shareholders’ value, and this point has been crossed way too many times.

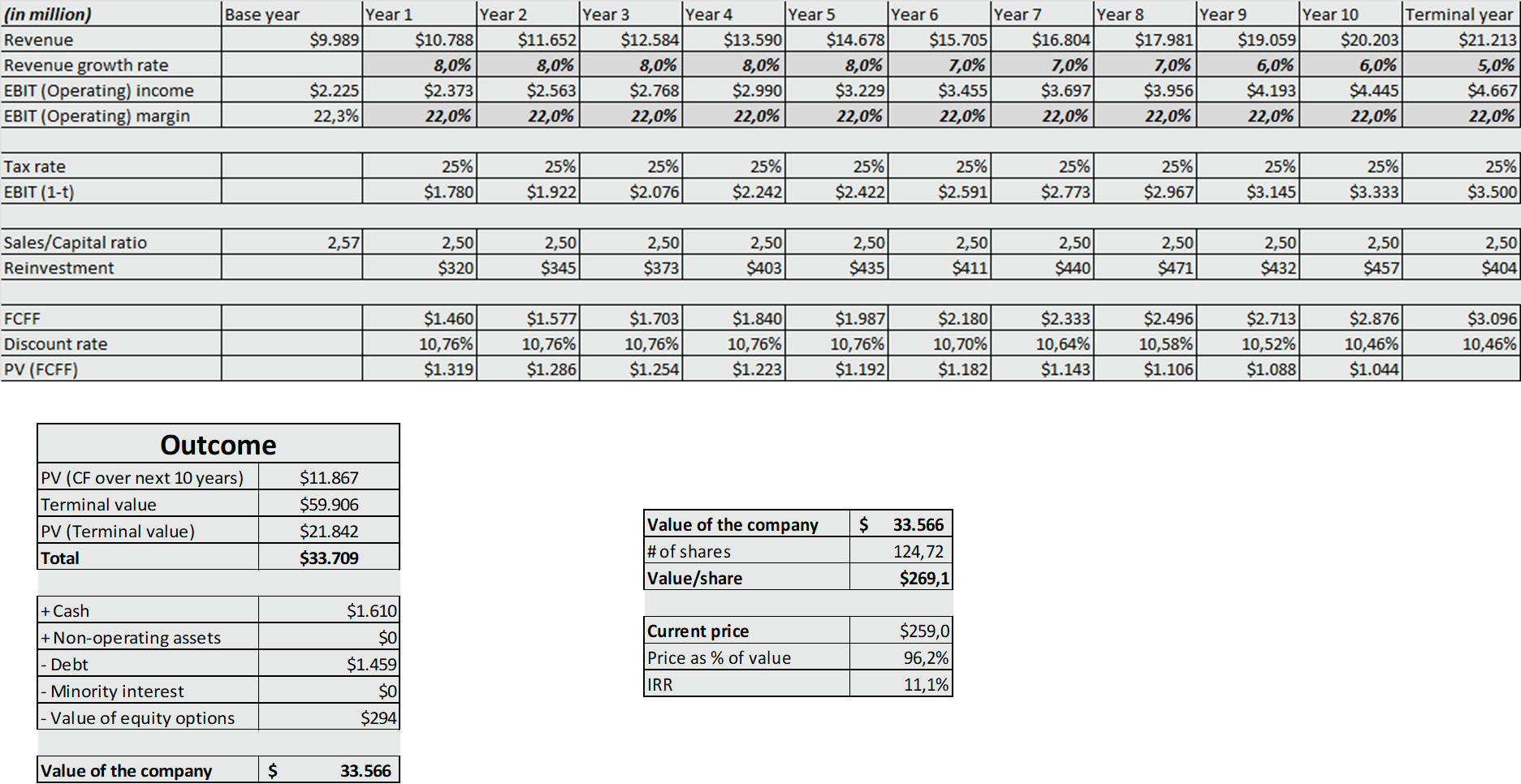

6.0 Valuation

Based on my assumptions, the fair value of the company is $33.6b ($269/share), not that far from today’s share price of $259.

Here’s how the valuation (per share) changes if you have different assumptions than mine regarding the revenue growth & the operating margin:

I hope you enjoyed this post, feel free to share your thoughts.

A great stock. A great review.

Agreed. FY27 FCF estimates are c. 1.5bn. That's 23x FCF. So likely fairly valued. The FCF estimates from FY24 to FY27 are largely similar. For the bulls this has to move upward to price the stock in the 350-400 USD range.