Deep dive into Michelin

The tire company that prints money

How does a company end up manufacturing tires and rating restaurants?

Here’s the story.

1.0 The beginnings

Edouard and Andre Michelin founded the company in Clermont-Ferrand in 1889, with the initial focus on rubber goods.

The demand for tires wasn’t high. There were bicycles and not too many cars.

With limited travelers, their question was, how do we encourage people to travel more, which would wear out their tires faster, and lead to Michelin selling more tires?

So they came up with the Guide. The first edition was published in 1900 and listed hotels, restaurants, mechanics, and gas stations. About 35,000 copies were given away, for free.

Over time, the restaurant section became quite popular they started recruiting professionals who would visit and review restaurants. In 1931, the 3-star system was introduced:

One star: A very good restaurant in its category.

Two stars: Excellent cooking, worth a detour.

Three stars: Exceptional cuisine, worth a special journey.

The Michelin Man is part of the company’s brand. In the early days of the company, the brothers were exhibiting their products at a fair when one of them noticed that if you added arms and legs to a pile of tires, it would look like a man.

This is one of the oldest trademarks still in active use, and according to the company, a study showed that 90% of the world’s population could instantly recognize it.

2.0 The transformation to today

In the 20th century, there was a lot of innovation, most notably, the steel-belted radial tire that Michelin commercialized ahead of the rest of the industry, and became the global standard.

Tires are everywhere, so there was also a push into specialty segments, such as mining, agriculture, and aircraft, where margins are higher as there’s less competition.

In 2018, Michelin acquired Fenner, a company specializing in conveyor belts.

In 2019, Michelin acquired Camso, a company specializing in off-road specialty tires and tracks.

In 2023, Michelin acquired Flex Composite Group, a European leader in engineered fabrics and films with applications in highly technical markets (marine, supercars, EVs, sports, and construction).

In 2026, there are 3 acquisitions, Cooley Group and Tex Tech Industries, both in coated fabrics and specialty textiles, and Flexitallic (expected to close H1-2026), specializing in sealing solutions.

The latest acquisitions are all about diversification (away from tires).

The company reports in three operating segments, but a fourth one will be introduced in 2026:

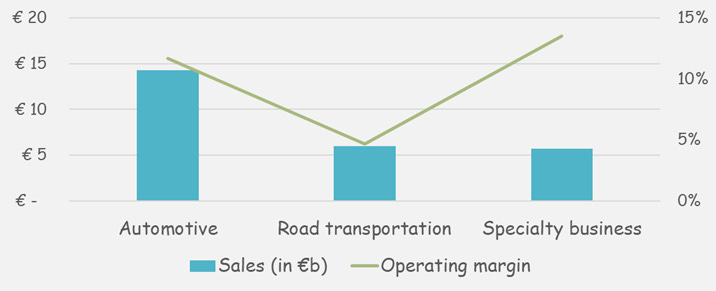

Automotive & Two-wheel: The core of the company, representing 55% of all sales. It covers passenger car, light trucks, and motorcycle/bicycle tires.

Road transportation: The next segment contributes 23% of all sales, and covers tires for heavy trucks, light commercial vehicles, buses, and connected fleet services.

Specialty (currently including the Polymer Composite Solutions - that will be a separate one as of 2026): Responsible for the remaining 22% of sales and is the highest-margin segment, as it covers mining tires, agricultural tires, construction tires, aircraft tires, etc.

The Polymer Composite Solutions (“PCS“) platform: This is the strategic diversification decision where many of the new acquisitions fall.

3.0 The risks

I think addressing the risks deserves a separate section, especially as there are 5 very important ones:

3.1 As shown on the above chart, this is not a high-margin business. Chinese tire manufacturers are exporting aggressively into European and North American markets at prices that premium brands cannot match. Currently, certain tariffs/duties are helping Michelin to remain competitive.

3.2 Dependency on manufacturers. When the manufacturing of European trucks or agricultural vehicles fell, it reflected in the demand for Michelin’s tires. Cycles like this do not last forever, but they can remain for a long time, harming the company’s margins.

3.3 PCS Integration is not risk-free. Each of the acquired companies is unique, and getting the most out of them isn’t an easy task.

3.4 Raw materials come with variable costs. In 2025, raw materials accounted for €5.1b of the direct costs, of which rubber was almost 50%.

(Side-note: The 2025 revenue was €26 billion)

Based on their notes, a $0.1 per kilogram change in natural rubber prices has an impact of $86 million (in one year).

The price has gone up about $0.5, which means the raw material cost would go up by ~$500m. The higher oil prices do not help either. It all depends on the company’s ability to pass the costs, but it is unlikely that 100% of that will happen. The H1-2026 margins will be lower, leading to lower FCF.

3.5 Lastly, there’s FX-impact. In the 16 months, this also harmed the company’s profit.

Almost all of the risks mentioned above have materialized, but it can always get worse.

4.0 The capital allocation

The company’s enterprise value is ~€24b (market cap of €22b + €2b of net debt).